Deep Dive: IREN Limited ($IREN)

From Bitcoin Miner to AI Infrastructure Powerhouse - And Why the Market Is Still Mispricing the Pivot

SPRINGBOK VERDICT

Rating: BUY

Current Price: $47 | Price Target: $86 | Upside: 83%

The Resignation

In 2018, two Australian brothers resigned from Macquarie Group - one of the world’s most prestigious infrastructure investment banks, and flew to the Canadian wilderness to mine Bitcoin.

Their colleagues thought they had lost their minds.

Daniel and Will Roberts did not look like crypto entrepreneurs. Between them they had spent the better part of a decade financing wind farms, pipelines, and toll roads. They understood how the physical world worked, and how to find cheap power, how to secure land, how to build large-scale facilities in remote locations, and how to make the economics work when margins were thin.

The idea was never really about Bitcoin.

The Thesis Nobody Believed

The Roberts brothers had watched the cloud computing buildout of the 2000s and noticed something most people missed. The companies that made the most enduring money were not the ones writing the software. They were the ones who owned the physical infrastructure the software ran on. Amazon Web Services was the most profitable business in the world not because Jeff Bezos invented cloud computing - it was because Amazon owned the physical layer everything else ran on top of.

The brothers believed something similar was coming for high-performance computing. Somewhere in the next decade there would be an explosion of demand for raw compute power. Whoever had the power, the land, and the data centers would be in the same position Amazon was in 2010.

They needed a first customer to pay the bills while they built. Bitcoin miners were perfect — price-indifferent to location, continuous 100% utilisation, and completely replaceable if something better came along.

The Crash

In late 2021 they took the company public on the NASDAQ, raising $232 million at a $1.5 billion valuation. Three months later, Bitcoin crashed 75%. The stock fell 95% - from over $20 to $1.02. Debt covenants were triggered. Creditors circled.

Daniel and Will Roberts did not sell.

They restructured, retained control of the core infrastructure, and kept the power contracts alive. The land was still there. The grid connections were still there. The data centers were still there. They had one belief that held through the worst of it, that the infrastructure was worth more than the Bitcoin price implied.

The Moment Everything Changed

In November 2022, OpenAI released ChatGPT. The world changed overnight.

Every technology company on earth was suddenly scrambling for the same scarce resource - high-density GPU compute, housed in data centers, connected to the grid. The hyperscalers had six-month waitlists. The startups had funding and nowhere to run their models.

IREN had 510 megawatts of data center capacity, cheap power contracts, and years of operational expertise running exactly the kind of infrastructure that AI workloads require.

The first customer to fully understand what IREN had built was Microsoft. In November 2025 they signed a $9.7 billion five-year contract, the largest single AI infrastructure deployment announced that year, with a 20% prepayment wired in advance. The company that came within weeks of losing everything in 2022 had just signed a $9.7 billion contract with the world’s second largest company.

Today IREN has 4.5 gigawatts of secured power, $9.2 billion in funding, and is targeting $3.7 billion in annualised AI Cloud revenue by end of 2026. The stock that bottomed at $1.02 hit an all time high of $76.87 before pulling back to approximately $42 today on broader market weakness.

The market is confusing a financing story with a fundamental one.

Two brothers. One thesis. Eight years of building. And a contract portfolio that makes the current valuation look like a rounding error.

That is where we begin.

What IREN Does

IREN is a vertically integrated data center company. That phrase gets used loosely in the industry so it is worth being precise about what it means in IREN’s case.

Vertically integrated means IREN controls everything from the ground up. The land. The power contracts. The data center design and construction. The cooling systems. The GPUs themselves. And the software layer that allows customers to access those GPUs remotely. Most competitors own one or two of these layers. IREN owns all of them.

That matters because each layer is a margin capture point. Every time a competitor outsources a layer, leases land instead of owning it, buys power at market rates instead of locking in long-term contracts, rents GPUs instead of purchasing them, they hand margin to someone else. IREN’s vertical integration means more of the economics stay inside the business.

The company runs two distinct revenue segments today with a third emerging.

Segment One - AI Cloud Services

This is the business IREN is becoming. Customers - AI companies, research labs, enterprises, all pay to access IREN’s GPU clusters by the hour or under long-term contracts. IREN provides the hardware, the power, the cooling, and the connectivity. The customer brings the workload.

The GPU fleet has grown from essentially zero eighteen months ago to approximately 100,000 units installed or on order as of December 2025, targeting 150,000 by end of 2026. The hardware is Nvidia’s latest generation, GB300s, B200s, and H200s - the same chips that every AI company in the world is competing to access.

The business model within AI Cloud has two flavours. Spot and on-demand pricing gives customers flexible access at market rates, higher margin when demand is strong but volatile. Reserved and contracted capacity locks customers into multi-year agreements at fixed pricing. The contracted model is where IREN is increasingly focused. The $9.7 billion Microsoft contract is the clearest expression of this. Five years, take-or-pay structure, 20% prepayment already received. That is not a rental business. That is a subscription business with a hyperscaler anchor tenant.

The economics of the contracted model are exceptional. Management has guided to an 85% EBITDA margin on the Microsoft project once fully commissioned. To put that in context — most SaaS businesses would consider 30% EBITDA margins aspirational. IREN is guiding to 85% on a multi-billion dollar infrastructure contract.

Segment Two - Bitcoin Mining

This is the business IREN was built on and the one the market still uses to price it. IREN operates 50 exahashes per second of Bitcoin mining capacity, one of the largest and lowest-cost operations in the world. The all-in electricity cost per Bitcoin mined runs at approximately $40,000–$42,000 against a current Bitcoin price of approximately $85,000. That is a hardware profit margin of roughly 75%.

The mining business does two things for the investment thesis. First it generates substantial ongoing cash flow, approximately $500 million in annualised hardware profit at current Bitcoin prices that funds the AI infrastructure buildout without requiring IREN to dilute shareholders at every turn. Second it provides operational leverage to the data center assets. The same power infrastructure, the same facility management expertise, the same grid connections that run the mining rigs are the foundation of the AI Cloud buildout. The mining business did not just fund IREN’s growth. It trained the team that is now deploying AI infrastructure at scale.

IREN has made clear it will not expand mining capacity beyond 50 EH/s. All incremental capital goes to AI. The mining segment is a cash engine, not a growth story.

Segment Three - AI Data Centers

Beyond its own GPU cloud business, IREN is developing purpose-built AI data centers for colocation - large-scale facilities that hyperscalers and enterprise customers can lease as physical space rather than purchasing GPU time. This is a higher-capital, longer-cycle business but it opens a second revenue model on the same physical assets.

The 750 megawatt Childress campus in Texas is the current operational center of gravity. The 2 gigawatt Sweetwater Hub, with substations targeting energisation in April 2026 and late 2027 is the next phase. And the 1.6 gigawatt Oklahoma campus announced in February 2026 extends the footprint further.

In total IREN has secured 4.5 gigawatts of grid-connected power across North America. In a world where power is the primary bottleneck for AI infrastructure, where substation lead times stretch years and grid connections in key US markets are essentially sold out - that 4.5 gigawatts is worth more than the current market capitalization reflects.

The Structural Advantage

Every layer of IREN’s business connects to a single underlying asset - cheap, renewable, grid-connected power in locations that most competitors arrived too late to access.

The Bitcoin mining background was not a detour. It was the training ground. Years of operating power-intensive facilities at scale, managing high-density computing environments, procuring energy at below-market rates, and building in remote locations, that expertise is now being deployed on a $9.7 billion Microsoft contract.

The market is still valuing IREN like a Bitcoin miner with an AI hobby. The fundamentals describe an AI infrastructure company with a cash-generative mining division. That gap is the investment thesis

Why We Are Bullish On IREN

The Demand Gap Is Structural…And Widening

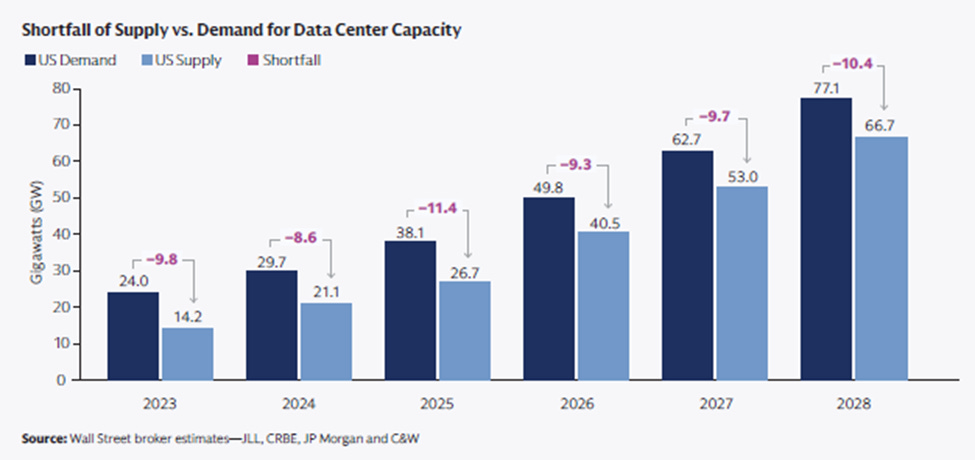

The numbers are unambiguous. In 2026, US data center demand is projected at 49.8 gigawatts against supply of 40.5 gigawatts, a 9.3 gigawatt shortfall. By 2028, that gap widens to 10.4 gigawatts. It does not close.

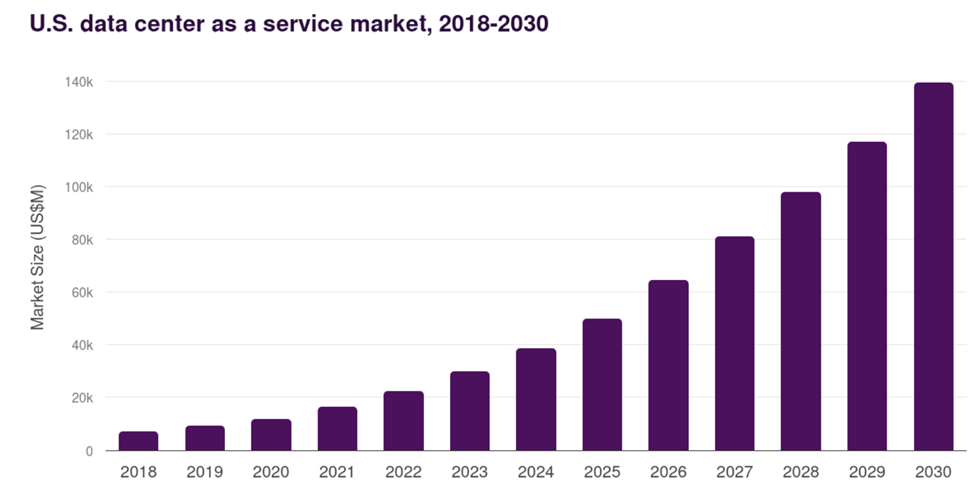

This is not a temporary imbalance that supply will eventually correct. It is a structural shortfall driven by a simple physical reality - building data center capacity requires power, and securing power requires grid connections that take years to negotiate, permit, and construct. The steepest part of the demand curve is ahead, not behind. The US data center as a service market is projected to grow from $38 billion in 2024 to nearly $140 billion by 2030, a near-quadrupling in six years.

IREN has 4.5 gigawatts of secured, grid-connected power across North America. In a market with a persistent double-digit gigawatt shortfall, that asset cannot be replicated by a competitor regardless of how much capital they deploy. Scarcity has a price. The market has not yet assigned it.

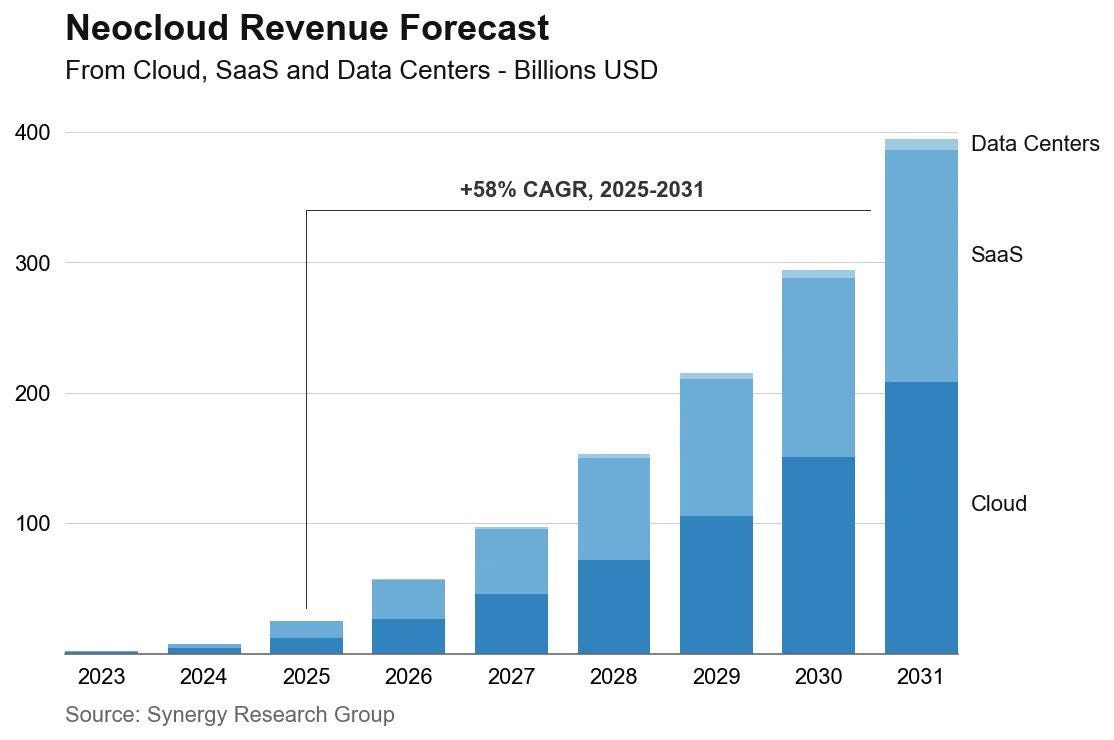

The Neocloud Market Is Growing At 58% Per Year

The neocloud revenue market, the direct addressable market for IREN’s AI Cloud business is forecast to grow at 58% CAGR from 2025 to 2031, reaching nearly $400 billion by end of decade, according to Synergy Research Group.

IREN’s $3.7 billion ARR target by the end of 2026 represents less than 4% of the total neocloud market in that year. The company does not need to compete with hyperscalers or dominate any segment. It needs to capture a single-digit percentage of a market that is doubling every 18 months, in a space where it already holds one of the scarcest inputs.

The Revenue Per Megawatt Transformation Is Not Priced In

One megawatt of power running Bitcoin mining generates approximately $2.9 million in annual revenue at current prices. One megawatt running contracted AI Cloud infrastructure generates $9.7 million, derived directly from IREN’s disclosed Microsoft contract of $1.94 billion ARR across 200MW of critical IT load.

Same land. Same grid connection. Same facility management expertise. More than three times the revenue.

IREN is systematically converting every available megawatt from the lower-value use to the higher-value one. As that conversion accelerates through 2026 and 2027, the revenue per megawatt of the business roughly triples. The market has not fully modelled what that transition means for the income statement.

Sweetwater Changes The Scale Of The Opportunity

IREN currently has 810MW of operational data center capacity. Sweetwater 1, with all four substation transformers now on site and energisation imminent, unlocks 1,400MW of additional capacity at a single site. Nearly doubling the operational footprint overnight.

At the Microsoft contract rate of $9.7M per MW per year, 1,400MW of fully contracted AI Cloud capacity implies an ARR ceiling that exceeds IREN’s entire current market capitalization. We model far more conservative numbers in our base case, but the illustration matters. The scale of what is being unlocked is not reflected in the current stock price.

The conversion of Sweetwater from secured to operational to contracted is the primary value creation event of the next 12 to 18 months. Energisation is the starting gun.

The Base Case Requires Only Execution

IREN has a $9.7 billion Microsoft contract, $9.2 billion in funding secured, and a 20% prepayment already received. The thesis does not require incremental contract wins beyond those modelled, multiple expansion, or margin improvement above our conservative 45% assumption.

It requires execution on infrastructure already built, against contracts already signed, with funding already secured.

At $47 per share, the market is pricing the financing overhang. It is not pricing the asset. That gap is where the opportunity lives

Valuation

We initiate coverage of IREN with a price target of $86/share, implying an upside of 83%.

We value IREN using a Sum of the Parts (SOTP) methodology, segmenting the business into its two distinct operating units - AI Data Center, Colocation and Bitcoin Mining, and valuing each independently based on its underlying economics. Given the capital-intensive, power-centric nature of IREN’s business model, we anchor our valuation to Enterprise Value per Megawatt (EV/MW) as the primary unit of analysis. This methodology reflects how institutional investors and M&A participants price data center and infrastructure assets in the current market, where power access is the primary value driver.

Segment One - AI Data Center

Revenue assumption: $7.5M per MW per year

IREN’s disclosed Microsoft contract, 200MW of critical IT load generating $1.94 billion in annualised run-rate revenue, implies a contracted rate of $9.7M per MW per year. We apply a conservative $7.5M per MW for forward projections, reflecting the expectation that incremental contracts will be priced below the Microsoft anchor rate as the mix shifts toward a broader, more diversified customer base.

EBITDA margin assumption: 75%

The management guided for an EBITDA margin of 85% in the Microsoft deal. We take a slightly conservative estimate of 75%.

EV/EBITDA multiple assumption: 6x

We apply a 6x EV/EBITDA multiple, a deliberately conservative assumption relative to comparable infrastructure operators. Equinix trades at approximately 24x. Digital Realty trades at approximately 20x. CoreWeave, as the most direct neocloud comparable, trades above 30x. We apply 6x to reflect IREN’s early-stage contracted revenue base, execution risk associated with the GPU deployment ramp, and the absence of a multi-year track record in AI Cloud operations. We expect this multiple to expand as the contracted revenue base diversifies and deployment milestones are met, but we do not build multiple expansion into the base case.

Segment Two - Bitcoin Mining

Revenue assumption: ~$900k per MW per year

At 67 EH/s, producing $37 per PH per day, generates a little more than $900k in yearly revenue.

EBITDA profit margin: 50%

Consistent with IREN’s reported Q1 and Q2 FY26 actuals, which recorded hardware profit margins of 50% at the Childress and British Columbia sites.

EV/EBITDA multiple assumption: 8x

The Bitcoin mining segment is valued at a lower multiple than AI Data Center, reflecting the commodity nature of mining revenue, sensitivity to Bitcoin price, and the company’s stated intent to cap mining capacity at 50 EH/s. The segment functions as a cash flow engine funding the AI transition, not as a growth asset.

Segment Three - AI data centers/colocation

Revenue assumption: $2.5M per MW per year

According to the CBRE report of 2025, the cost of renting at centers in North America was $190/kw/month. This comes at $2.28M/MW/year. We round it up to $2.5M as IREN’s data center are some of the ebay, with modern cooling.

EBITDA profit margin: 80%

Major cost for IREN is electricity for running the data cente.r 80% remains a conservative estimate in this case.

EV/EBITDA multiple assumption: 8x

Value at 8x multiple as this segment does not generate much debt and provides constant cash flows.

Springbok Verdict

Our price target of $86 is derived from conservative assumptions at each stage of the model, a revenue rate at half the disclosed Microsoft contract level, an EBITDA margin below mature peer levels, and an EV/EBITDA multiple at a significant discount to every comparable infrastructure operator. The target does not require multiple expansion, margin improvement, or incremental contract wins beyond those already modelled. It requires execution on infrastructure that is already built, against contracts that are already signed.

Sensitivity to key assumptions is material. A re-rating of the AI EV/EBITDA multiple from 6x to 8x, still well below any comparable, would add approximately $9.4 billion to enterprise value, implying a price target of approximately $90. A margin expansion from 45% to 50% at the same 6x multiple would add approximately $3.5 billion, implying a price target of approximately $76.

The base case is the floor

Risks

1. Capital Management & Dilution IREN has a $6 billion ATM equity facility outstanding. Aggressive share issuance to fund the AI buildout could materially dilute existing shareholders. At 332 million shares today, the fully diluted count could approach 450 million by end 2027. compressing per-share value even if the business performs.

2. GPU Deployment Delays The $3.7 billion ARR target assumes on-time delivery and commissioning of GPUs across multiple sites. Any delay in hardware delivery, liquid cooling installation, or data center construction directly delays revenue recognition. The Microsoft contract is phased through 2026, slippage on any phase compresses near-term ARR.

Our View

IREN is not a complicated story. It is a simple one that the market has not yet finished reading.

Two brothers spent eight years building infrastructure that nobody wanted, and ended up with exactly what the world needs most. Cheap power. Grid connections. Data centers. The physical foundation of the AI economy, assembled quietly while everyone else was looking at software.

The Bitcoin crash that nearly killed the company in 2022 turned out to be the best thing that could have happened to the thesis. It forced discipline. It kept the balance sheet lean. It proved that the Roberts brothers would not walk away when things got hard. The infrastructure survived. The team survived. The conviction survived.

Today IREN has a $9.7 billion Microsoft contract, 4.5 gigawatts of secured power, and a revenue model that generates nearly ten times more per megawatt than the Bitcoin mining business it is replacing. The market is still pricing it like a crypto company. The fundamentals describe something entirely different.

At approximately $47 per share against our base case price target of $86, the implied upside is 83%. That is not a heroic assumption. It is what you get when you apply a conservative 6x EV/EBITDA multiple to contracted revenue that Microsoft has already prepaid for.

The thesis is being executed now. The demand is signed. The power is secured. The capital is funded. What remains is delivery, and the team that built one of the world’s largest Bitcoin mining operations from scratch in the Canadian wilderness has demonstrated, repeatedly, that delivery is what they do.

We are long IREN.