Deep Dive: Micron ($MU)

AI arms race runs through Boise, Idaho

SPRINGBOK VERDICT

Rating: BUY

Current Price: $433 | Price Target: $606 | Upside: 40%

The $5.8 billion bleed

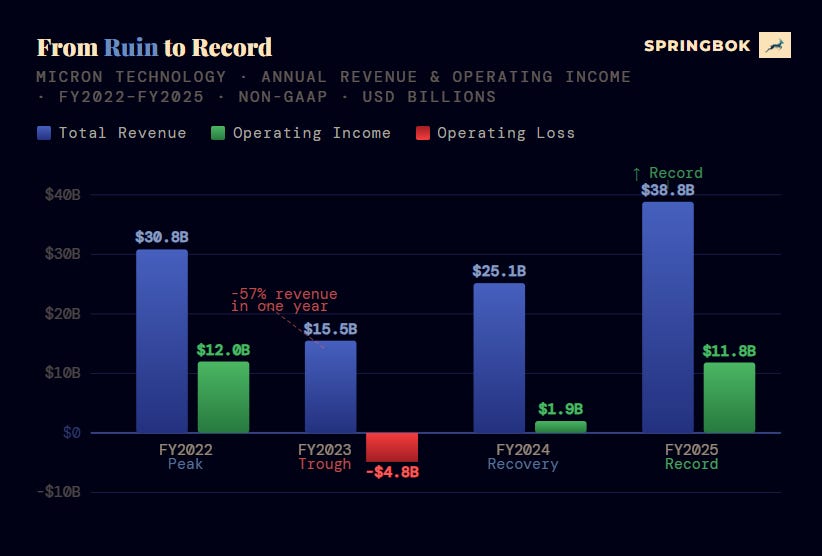

In the fiscal year ending August 2023, Micron Technology lost $5.8 billion.

Not a rounding error. Not an accounting quirk. Five point eight billion dollars - on $15.5 billion in revenue that had collapsed 57% from the year before.The company that had spent decades clawing its way into the upper tier of global semiconductor manufacturing was haemorrhaging cash. Layoffs followed. Capital expenditure was slashed. The mood in Boise was not optimistic.

Wall Street had an explanation ready. Memory is a commodity business. Cycles happen. DRAM prices collapse, companies bleed, eventually supply adjusts and prices recover. Nothing structural. Nothing interesting. Come back in two years.

Most investors did exactly that. They looked away.

That was the mistake.

The Silent Pivot

Because while the analysts were busy explaining why memory was uninvestable, something was changing underneath the surface. The AI buildout, quietly accelerating through 2023, and then exploding into public consciousness with every new model release - was creating a category of memory demand that never existed before.

Not commodity DRAM for laptops and servers. Something faster, denser, more power-efficient, and radically more expensive. Something that required years of process development to manufacture at yield.

Micron’s engineers had been working on that exact problem since 2021.

By the time the world caught up to what HBM was and why it mattered, Micron had already done the hard work. The yields that analysts had written off as permanently impaired were improving. Qualification timelines with hyperscalers were compressing (the testing process before a customer commits to buying at scale). And the customers who had spent 2023 avoiding memory suppliers were coming back - urgently, and with open chequebooks.

From Ruin to Record

The numbers that followed are almost disorienting to read alongside the 2023 results.

Fiscal 2025 revenue: $38.8 billion. Up 61% year over year. A record.

Operating income: $11.8 billion, versus an operating loss of $5.7 billion just two years prior.

2026 HBM supply: fully contracted. Every unit already spoken for.

Capex guidance raised to $20 billion - with the increase directed explicitly at HBM supply capability.

The Idaho fab, originally scheduled for later in the decade, has been pulled forward to mid-2027. A second Idaho facility has broken ground.

This is not a cyclical recovery. Cyclical recoveries don’t come with multi-year contracted supply and accelerated construction timelines. This is a company that walked into the most important memory transition in a generation and emerged as one of three suppliers on earth capable of meeting demand.

The Geopolitical Ace

There is one dimension of this story that gets almost no coverage.

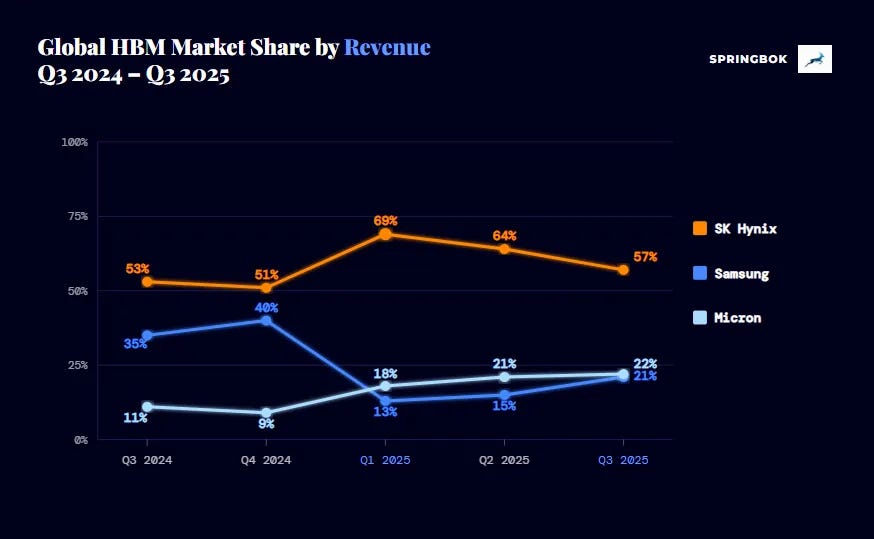

Micron is the only US-domiciled High Bandwidth Memory manufacturer on the planet. SK Hynix is Korean. Samsung is Korean. The entire HBM supply chain - the infrastructure that every American AI company depends on to train and run its models runs through Seoul. Except for one company in Boise, Idaho.

And Washington took notice. The CHIPS Act directed $6.1 billion toward Micron specifically. Not as a subsidy but as a strategic imperative.

In a world where semiconductor supply chains have become a matter of national security, being the only American option is not a footnote in the investment case.

It is the investment case.

What Micron Actually Makes

Micron is a two-product company. Everything it sells is either DRAM or NAND. Two types of memory, two different jobs, two very different market dynamics.

Understanding both is the foundation of the entire investment case.

DRAM - The Memory That Thinks

DRAM is short-term memory. It holds the data a processor is actively working with the information that needs to be accessed instantly, thousands of times per second.

Every time you open an app, stream a video, or ask an AI model a question, DRAM is what the processor is reaching into. Without enough of it, everything grinds to a halt. There is no workaround.

It is also Micron’s most important business. DRAM generates roughly 76% of total revenue and virtually all of the earnings leverage when the cycle turns. In FY 25, DRAM revenue came in at $28.6 billion. By FY 26, our model projects that figure reaching $76.4 billion, a 167% increase in a single year.

Standard DRAM comes in several forms - DDR5 for servers, LPDDR5X for smartphones, DDR4 for legacy infrastructure. These are commodity products. High-volume, price-sensitive, and cyclical. They are what most investors think of when they think of Micron.

But inside DRAM, something has emerged that is changing the economics of the entire segment.

High Bandwidth Memory (HBM)

Standard DRAM has a problem. It sits beside the processor, connected by a memory bus - a channel with hard physical limits on speed and capacity. Engineers called this the memory wall. For decades, they patched around it. Wider buses. Higher frequencies. Incremental fixes.

HBM solves it differently.

Instead of sitting beside the processor, HBM dies are stacked vertically - one on top of another, connected through thousands of microscopic copper pillars punched directly through the silicon. Data no longer travels centimeters across a circuit board. It travels micrometers through a stack.

The result: 4x the bandwidth. Lower power consumption. And a price per gigabyte that is 5 to 8 times standard DRAM - reflecting the extraordinary complexity required to manufacture it.

The demand driver is simple and non-negotiable.

Every new generation of Nvidia GPU requires significantly more HBM than the last. The H100 shipped with 80GB. The Blackwell B200 with 192GB. The Rubin platform targets 288GB per chip - a 260% increase over the H100 in a single GPU generation. That is not linear demand growth. It is exponential - locked in by the architectural decisions of the world’s most important chip designer. The total HBM market is projected to reach $100 billion by 2028, growing at roughly 40% annually.

Micron was late to HBM. Its HBM3E yields trailed SK Hynix. The bear case was loud and widely held.

Then HBM4 arrived - and the race reset.

Micron’s HBM4 is ramping in Q2 2026 with industry-leading speeds above 11 Gbps. And Micron is currently meeting only 55 to 60% of core customer demand.

Not because the product is weak. Because the fabs cannot build it fast enough.

Being supply-constrained in a market growing at 40% annually is not a problem. It is a pricing environment.

NAND - The Memory That Stores

Where DRAM holds data being actively used, NAND holds data at rest.

Everything that needs to be kept but is not being processed right now. This includes the files, the models and the training datasets. It is the technology inside every SSD, every smartphone, and every enterprise storage system on the planet.

NAND is a harder business than DRAM. More commoditised, more competitive, and historically more prone to oversupply. The 2023 downturn hit NAND harder - prices fell further, and the recovery came slower. At the trough, Micron’s NAND revenue dropped to under $1.9 billion in a single quarter.

But two things are changing.

The first is AI storage demand. Training a large language model requires petabytes of data. Running inference at scale requires fast local storage at every node in the cluster. The shift from mechanical hard drives to enterprise SSDs is accelerating - and Micron’s 232-layer NAND process is competitive enough to capture a meaningful share of that shift. NAND revenue is projected to grow from $8.5 billion in FY 25 to $17.4 billion in FY 26 as enterprise SSD volumes scale.

The second is QLC NAND - quad-level cell technology that stores more data per cell, delivering higher density at lower cost. Micron has been more aggressive than peers in pushing QLC into enterprise storage. That bet is now paying off.

NAND is not the reason to own Micron. But it is no longer the drag it was in 2023. A recovering market, growing enterprise SSD demand, and a maturing QLC strategy, layered on top of a structurally repriced DRAM business. This creates the operating leverage the current valuation does not fully reflect.

The Geographical Moat - The Advantage Nobody Can Buy

Here is the part of the Micron story that most analysts mention briefly and then move past. It deserves more than a footnote.

SK Hynix is Korean. Samsung is Korean. Between them, they control the overwhelming majority of global HBM supply. Every American hyperscaler - Google, Microsoft, Amazon, Meta along with every American AI company training models and running inference at scale, depends on fabs in Seoul for the memory their infrastructure runs on.

Micron is from Boise, Idaho.

That geographic fact, which once seemed irrelevant to the investment case, has become one of the most strategically significant details in the entire semiconductor industry.

Washington took notice of this. The CHIPS Act directed $6.1 billion specifically toward Micron - not as a subsidy for a struggling company, but as a strategic investment in domestic semiconductor sovereignty. The calculation in Washington is straightforward: if Korean fabs go offline for any reason - geopolitical escalation, natural disaster, supply chain disruption - the American AI industry loses access to its most critical memory input. That is not an acceptable risk.

Micron is the answer to that risk. The only one.

Samsung and SK Hynix can match Micron on technology. They can compete on price. They can win qualification cycles. But they cannot move their fabs to Idaho. The geographical moat is permanent - and in the current geopolitical environment, it is becoming more valuable every year.

Why We Are Bullish On Micron

The thesis is simple. Prices are rising. Supply cannot keep up. And Micron captures every dollar of that gap directly in its margins.

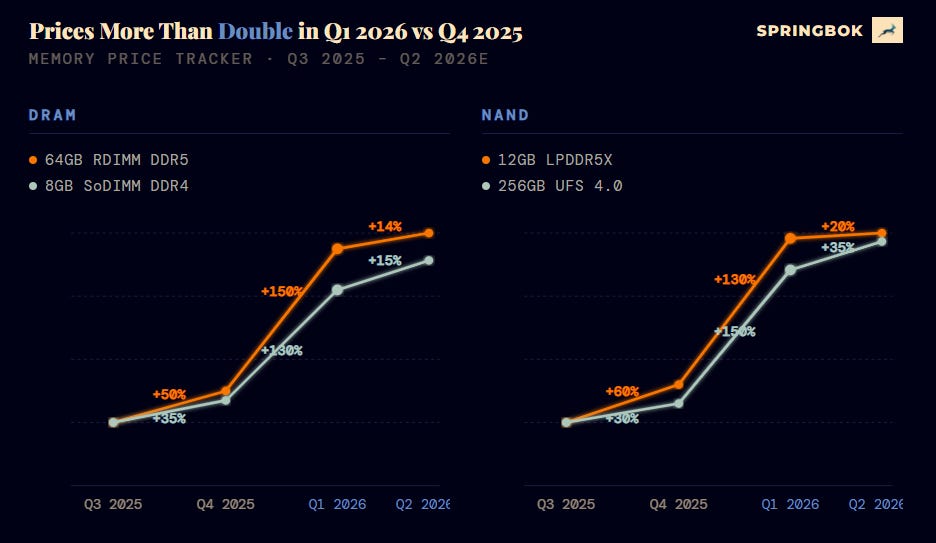

Prices Are Not Recovering. They Are Exploding.

Let’s be precise about what is happening here, because the word “recovery” does not do it justice.

DRAM prices rose 130% between Q4 2025 and Q1 2026. Not over a cycle. Not over a year. In a single quarter. NAND moved the same distance in the same window. To put 130% into perspective, a 5% quarterly jump in prices is considered a huge win in most industries.

These are not the gradual price improvements of a market finding its footing. These are the price movements of a market in structural undersupply, where buyers are competing for a product that does not exist in sufficient quantity at any price.

To put that in context: the customers who were practically giving memory away eighteen months ago are now signing multi-year contracts to secure supply they are not sure they can get. The dynamic has inverted completely.

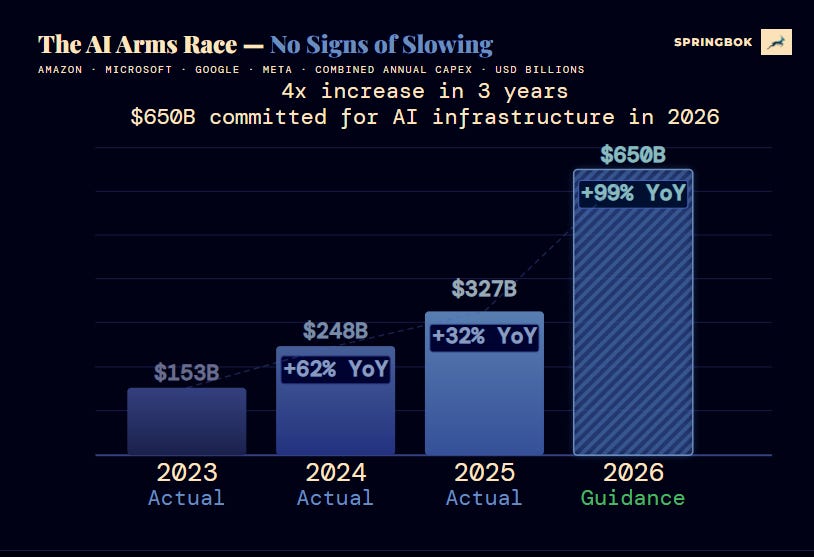

The mechanism is not complicated. AI infrastructure spending did not slow down when memory prices started rising. It accelerated. Every new data center that Nvidia, Microsoft, Google, and Amazon are building requires more DRAM, and specifically more HBM, than the last. The demand curve moved sharply upward. The supply curve, constrained by qualification timelines, fab capacity, and the extraordinary complexity of HBM manufacturing, could not follow. The gap between those two lines is where the margin expansion lives.

Source - Marvell technology Custom AI Investor Event

For Micron, this is not an external tailwind. It flows directly into the income statement. When DRAM prices rise 130% in a quarter, and you are one of three companies on earth that can supply the product, the operating leverage is extraordinary. Gross margins moved from 39% in Q1 FY2025 to nearly 57% by Q1 FY2026 - and our model projects them reaching 73% by FY 27 as pricing power for Micron rises.

This is the trade.

Valuation

We initiate coverage of Micron Technology with a price target of $606 per share, representing 40% upside to the current price of $433. Verdict: BUY

The stock has re-rated over 300% from its 2023 trough. Despite this, we believe the market has priced in only the cyclical recovery - and has not yet reflected the structural repricing underway in both DRAM and NAND. Our target is not predicated on multiple expansion. It is predicated on earnings delivery.

Key assumptions:

Multiple compression, not expansion. We apply a 7x two-year forward P/E, a deliberate compression from the current 11x. In simple terms, we are being deliberately conservative. Every assumption in this model is built to understate the opportunity, not overstate it.

A two-segment revenue model. The model is a two-segment business. Micron generates revenue in DRAM and NAND. In both segments, revenue is simply price multiplied by volume. We track quarterly price movements through ASP and volume growth through bit growth. ASP - Average Selling Price - measures what is the change in the price per unit with respect to last quarter. Bit growth measures how many units it sells. Revenue is simply one multiplied by the other.

Earnings driven by price, amplified by operating leverage. EPS expanded from $8.29 in FY 25 to $86.58 in FY 27, primarily reflecting the sharp recovery in DRAM and NAND pricing. This expansion is further amplified by a cost base that does not scale linearly with revenue, producing gross margin progression toward 73% as contracted HBM volumes scale.

Price target of $606 on 7x FY2027 earnings. For a business compounding earnings at this trajectory, a 7x exit multiple is not optimistic. It is conservative.

Risks

Slowdown in AI Infrastructure Spending - The entire demand thesis rests on continued AI capital expenditure from hyperscalers. If spending is recalibrated, DRAM demand softens quickly and prices follow.

Micron operates in one of the most geopolitically exposed industries on the planet - with meaningful revenue concentration in China, and critical supply chain dependencies in Taiwan and South Korea. A Beijing escalation, Taiwan Strait disruption, or shift in US trade policy could affect production, revenue, or capital plans.

HBM4 Yield Disappointment - Micron’s competitive repositioning rests entirely on HBM4 ramping on schedule with competitive yields. A disappointment would not just impair near-term revenue - it would lose market share to its competitors.

TLDR Version

Micron makes the memory that powers every AI model on the planet. Because of AI driven demand, the price of that memory just jumped 130% in a single quarter - and the stock has not caught up yet. With AI infrastructure spending accelerating and supply unable to keep pace, that pricing power is not going away. We see 40% upside from here with a target price of $606/share.

Every position and price target will be tracked publicly. Nothing here is financial advice - do your own work, but we’ll show you ours.

If you found this useful, the best thing you can do is share it with someone who’d enjoy it. These essays take time to put together, your share is what makes them sustainable.