Deep Dive : SanDisk Corp ($SNDK)

The stock went up 40x because of what it earned last year. What it earns next year makes today look cheap.

SPRINGBOK VERDICT

Rating: BUY

Current Price: $1,559 | Price Target: $3,983 | Upside: 155%

The Man Who Refused To Accept That Storage Had Limits

In 1973, a young Israeli physicist named Eli Harari completed his PhD at Princeton and joined Hughes Aircraft. While studying electronic tunnelling in ultrathin dielectric films, the kind of research that sounds incomprehensible to anyone outside a laboratory - he made a discovery that would eventually change how every piece of digital information on earth is stored.

He invented the Floating Gate EEPROM, the first practical electronically erasable programmable read-only memory, which paved the way for today’s entire flash memory industry.

Hughes Aircraft did not know what to do with it. Neither did most of the industry.

Harari spent the next fifteen years watching his invention gather dust while the world stored data on magnetic disks, tape reels, and spinning hard drives - technology that was bulky, fragile, power-hungry, and fundamentally mechanical. Every time a hard drive failed, somewhere in the world a physicist was quietly certain there was a better way.

In the second half of 1988, working from a small office in Palo Alto, Harari wrote a business plan for a company that would commercialise flash memory at scale. In January 1990, just fifteen months after founding the company, he gave an invited talk at IEEE Santa Clara where he described future applications of flash memory in cell phones, digital cameras, and portable devices. There was no email. The smartphone did not exist. Digital cameras were a laboratory curiosity.

He was describing a world that would not arrive for another decade.

Harari co-founded SunDisk, later renamed SanDisk - in 1988 with Sanjay Mehrotra and Jack Yuan, to pursue his vision of a system-level architecture that would successfully overcome the fundamental physical limitations of flash EEPROM transistors.

In 1991, SanDisk produced the first flash-based solid-state drive for IBM, 20 megabytes in a 2.5-inch form factor, priced at approximately $1,000. Twenty megabytes. One thousand dollars. The product was technically extraordinary and commercially absurd. Nobody bought it.

SanDisk’s engineers did not stop. They went back to the laboratory and did what semiconductor engineers do - they made it smaller, faster, cheaper, and more reliable. Year after year. Over two decades they drove down the cost of flash memory by more than 100,000 times through Moore’s Law scaling and a SanDisk invention called Multi-Level Cell technology, which allowed two or three bits of data to be stored on each flash transistor.

The SD card. The CompactFlash card. The USB drive. The SSD in your laptop. The storage in your iPhone. Every piece of portable storage that has defined the last thirty years of computing traces back to a small office in Palo Alto in 1988, where a physicist with a theory nobody understood decided to build a company around it anyway.

In 2016, Western Digital acquired SanDisk for $19 billion. The inventor’s vision, built over nearly three decades, had created one of the most important technology companies in the world.

Then Western Digital absorbed it, bundled it with a declining hard drive business, and spent nine years making it invisible.

In February 2025, SanDisk was spun off again. Independent. Pure-play. Free.

It opened at $38.50.

Fifteen months later it is at $1559. And we think the re-rating is not finished. Here is why.

The story earns every word. A Princeton physicist invents the technology in 1973, spends fifteen years watching it ignored, founds a company in 1988 that nobody believed in, builds the product for $1,000 that nobody bought, drives the cost down 100,000 times over two decades, creates a $19 billion company and then watches it disappear inside a conglomerate for nine years before being set free.

That is the SanDisk story

What SanDisk Does

SanDisk makes one thing. NAND flash memory.

Not DRAM. Not HBM. Not logic chips. Not processors. Every engineer, every dollar of capital expenditure, every management decision at SanDisk is directed at a single technology and that singular focus is precisely what makes it interesting.

NAND is the memory that stores data permanently. It is in your phone, your laptop, your camera, and every data center running AI workloads. Unlike DRAM, which holds data temporarily while a processor is working on it, NAND holds data when the power is off. Every AI model trained, every dataset stored, every inference output saved - all of it lives on NAND.

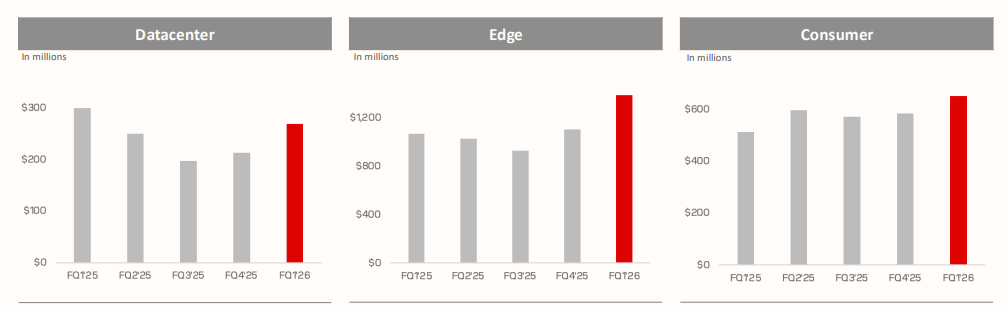

The applications span the full spectrum of computing. At the consumer end, SanDisk supplies the SD cards, USB drives, and portable storage that made the brand a household name over three decades. At the enterprise end, which now represents the majority of revenue and virtually all of the growth, SanDisk supplies high-capacity, high-performance solid-state drives to hyperscalers, AI companies, and data cents running the infrastructure that the intelligence economy depends on.

These enterprise drives are designed for AI data lakes, allowing data centers to consolidate dozens of racks into a single unit, drastically reducing energy consumption and cooling costs. A single large language model training run can consume petabytes of storage. Multiply that across thousands of concurrent training runs at every major AI lab and hyperscaler, and the storage requirement becomes staggering. NAND is not a peripheral component of the AI buildout. It is foundational infrastructure.

The manufacturing foundation underneath all of this is the joint venture with Kioxia - formerly Toshiba Memory, which together holds approximately 35% of global NAND manufacturing capacity. This joint venture, built over 25 years of collaboration, is the most important structural fact about SanDisk’s competitive position. NAND manufacturing requires years of process development, billions in capital expenditure, and specialised expertise that cannot be replicated quickly. A new entrant would need a decade and $20 billion to reach competitive scale. The Kioxia relationship is a moat that does not appear on the income statement but underlies every margin and cost advantage the company has.

By controlling the technology from wafer fabrication through its Kioxia joint venture to final product assembly, SanDisk maintains high vertical integration, allowing it to capture margins that fabless competitors cannot.

SanDisk currently holds approximately 13% of the global NAND market. While it ranks fifth in total volume, it is increasingly seen as the most agile player in the high-margin enterprise segment. The other major NAND players, Samsung, SK Hynix, Micron, Kioxia, all manage NAND as one division within broader semiconductor portfolios. Samsung is simultaneously managing a massive DRAM business, an HBM ramp, and a foundry operation. SK Hynix is focused heavily on HBM. Micron is balancing DRAM and NAND simultaneously.

SanDisk has no such distraction. When enterprise customers need a storage partner who can commit fully to long-term supply agreements, customised product development, and deep qualification cycles, a pure-play is structurally more committed than a division of a conglomerate managing a dozen other priorities.

That is the SanDisk business. Simple. Focused. And increasingly irreplaceable to the customers who depend on it

Why We Are Bullish On SanDisk

1. The Demand Is Not Linear. It Compounds.

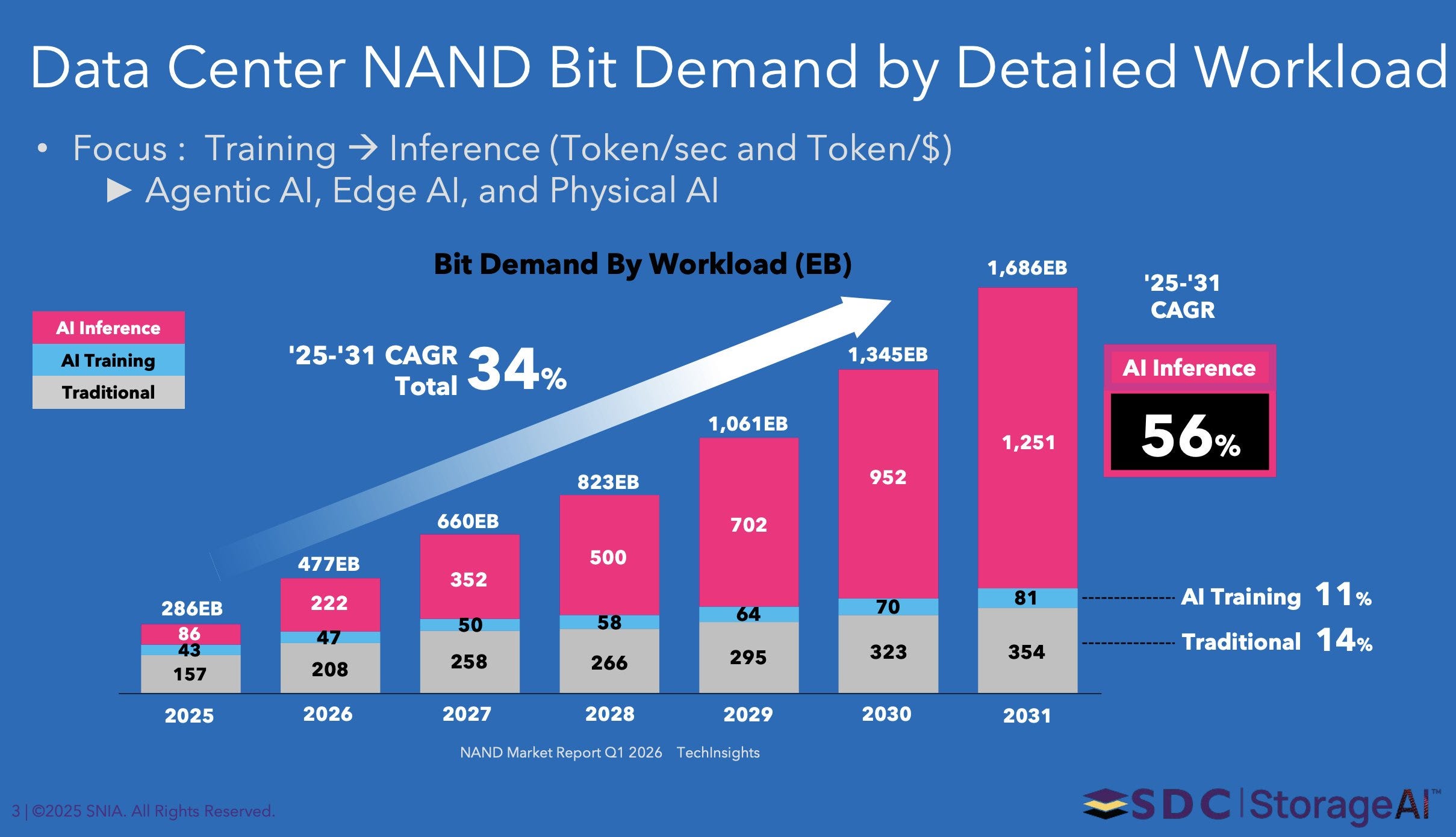

The NAND bit demand chart above is the most important slide in the industry right now.

Data center NAND bit demand is growing at 34% CAGR from 2025 to 2031 - from 286 exabytes today to 1,686 exabytes by end of decade. But the composition of that growth is what makes it structurally different from every previous NAND cycle.

In 2025, AI inference consumed 86 exabytes - 30% of total data center NAND demand. By 2031, AI inference alone consumes 1,251 exabytes, growing at 56% CAGR. The key insight is this: the AI shift from training to inference changes the NAND demand profile permanently. Training runs happen periodically. Inference runs happen continuously, every query, every user interaction, every API call is an inference event that requires storage access in real time. As AI moves from the laboratory into production, into every app, every enterprise workflow, every consumer product, inference becomes the dominant workload. And inference is far more storage-intensive per dollar of compute than training.

The demand curve does not flatten. It accelerates. Jevons Paradox is operating in real time - token prices have fallen 60% since late 2024 while token demand has increased 10x in the same period. Cheaper AI does not reduce infrastructure demand. It expands it.

2. The Revenue Opportunity Is Measured In Hundreds Of Billions

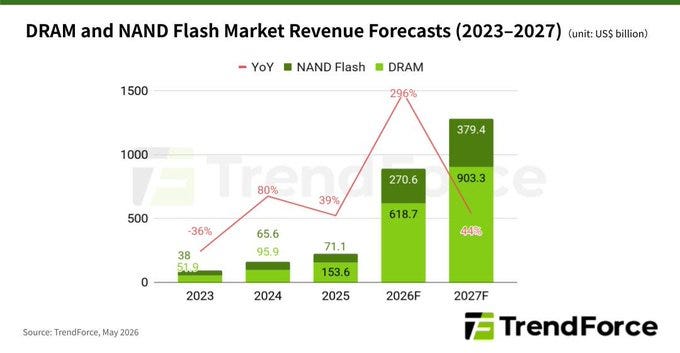

The TrendForce chart translates the bit demand story into revenue. NAND Flash market revenue is forecast to reach $270.6 billion in 2026, up 296% year over year. By 2027 it reaches $379.4 billion.

SanDisk holds approximately 13% of global NAND market share. At 13% of a $379 billion market, the implied revenue opportunity by 2027 is approximately $49 billion, against full year FY25 revenue of $7.4 billion.

Fiscal 2026 EPS is anticipated to be $50.53, a 2,738% year-over-year jump, followed by a further 164.9% annual rise to $133.84 in fiscal 2027. The market is growing faster than anyone expected twelve months ago. The 296% year-over-year revenue growth forecast for 2026 is driven by a genuine structural surge in enterprise and data center demand that traditional consumer-centric NAND models never anticipated.

3. The Five Long-Term Agreements Change The Business Model

For thirty years the NAND industry operated without long-term supply agreements. Customers bought on the spot market. When demand dropped, prices crashed. The cycle was reliable, brutal, and completely unpredictable - and it is the primary reason memory stocks have historically traded at depressed multiples.

SanDisk has done something no NAND company has done before at scale. Five long-term supply agreements - New Business Model contracts, with financial penalties for cancellation. $42 billion in minimum contracted revenue backlog. $11 billion in enforceable financial guarantees backed by third-party financial instruments. Over a third of FY27 bit supply was already sold before the year had begun.

This changes the fundamental nature of the business in two ways. First, it dampens cyclicality, the portion of revenue under long-term contracts is insulated from spot market price movements. Second, and more importantly, it justifies a structurally higher valuation multiple. The market applies a commodity discount to commodity businesses. A business with $42 billion in contracted revenue backlog and penalty-protected supply agreements is not a commodity business. It is an infrastructure franchise. Infrastructure franchises trade at infrastructure multiples.

4. Supply Remains Structurally Constrained

SanDisk’s own 10-Q states that demand for NAND continues to outpace supply and that the company expects this imbalance to persist through calendar year 2026.

This is not a bullish analyst making an optimistic forecast. It is the company itself, in a legal filing, describing the supply-demand environment. Building new NAND manufacturing capacity requires two to three years of construction, equipment installation, and process qualification before a single wafer reaches production. The demand surge that began in 2024 cannot be met by supply additions until 2027 at the earliest - and even then, the AI inference demand curve suggests demand will have grown faster than supply by the time it arrives.

Pricing power in a supply-constrained environment flows directly to margins. SanDisk’s Q3 gross margin of 78.4%, above Apple’s is the result of that pricing power. The supply constraint that produced it has not been resolved.

5. QLC Stargate, The Revenue Catalyst That Has Not Yet Started

SanDisk’s QLC Stargate platform is emerging as a powerful new revenue catalyst, with the company expecting revenue-generating shipments to begin in Q4 FY2026. The launch strengthens SanDisk’s position in the rapidly expanding AI-driven data center storage market and creates an additional growth avenue beyond its already successful TLC enterprise SSD portfolio.

QLC stores four bits of data per cell rather than three, meaning more storage density per wafer and lower cost per gigabyte for hyperscalers building AI data lakes. As enterprises and hyperscalers deploy larger AI models, Retrieval-Augmented Generation applications, KV cache technologies, and agentic AI systems, demand for high-capacity, cost-efficient flash storage continues to rise.

The critical point: QLC Stargate has not contributed a single dollar of revenue to SanDisk’s income statement yet. The 233% data center revenue growth in Q3 was achieved entirely on the existing TLC product line. Jefferies specifically identified forthcoming QLC eSSD deliveries to two major cloud providers as a potential catalyst for expanding data center market share.

Stargate is incremental upside that begins in Q4, and the current consensus has not fully modeled it. The best revenue catalyst in SanDisk’s pipeline has not yet shipped.

Valuation

We value SanDisk Corp at $3,983/sh, implying an upside of 155% against current stock price of $1559/sh.

Valuing SanDisk requires a clear-eyed acknowledgement of where we are in the NAND cycle and a decision about how much of the current shortage environment to embed in forward projections.

Our answer is straightforward. The shortage is real, documented in SanDisk’s own SEC filings, and confirmed by TrendForce’s supply-demand analysis. We model it persisting through 2026 and into early 2027,consistent with management guidance and the structural reality that new NAND manufacturing capacity takes two to three years to bring online. We do not model it lasting forever. The cycle will eventually turn. But the turn is not imminent, and the earnings power being generated in the meantime is extraordinary.

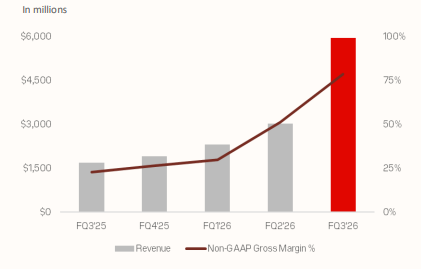

The Building Blocks

Our model runs from Q3 FY25 through Q4 FY27, anchored to five quarters of reported actuals and extended forward using two drivers: ASP trajectory and bit shipment growth.

The actuals require no explanation. Revenue grew from $1,695 million in Q3 FY25 to $5,950 million in Q3 FY26, a 251% increase in five quarters. Gross margin expanded from 23.7% to 78.4% in the same period. EPS moved from -$0.30 to $23.41. These are not projections. They are reported numbers. The business is already generating earnings at a pace the current stock price has not fully caught up with.

The forward projections embed two assumptions that require explicit justification.

ASP assumption: We model 40% sequential ASP increase in Q1 FY27, moderating to 30% in Q2, 20% in Q3, and 5% in Q4. This is aggressive in absolute terms. It is defensible in the context of a severe NAND shortage, the same shortage that produced 78.4% gross margins in Q3 FY26, that SanDisk’s management described in legal filings as expected to persist through calendar 2026, and that produced $42 billion in contracted revenue backlog from hyperscalers willing to pay financial penalties for supply certainty. DRAM ASPs moved comparably during the 2017-2018 shortage cycle. The NAND shortage of 2025-2026, driven by structural AI demand rather than cyclical consumer demand, is more durable.

Bit growth assumption: We model 5% sequential bit growth in Q1 and Q2 FY27, accelerating to 10% in Q3 and 12% in Q4 as QLC Stargate shipments ramp and the Kioxia joint venture increases output. These are conservative relative to historical ramp rates at comparable points in previous shortage cycles.

The Valuation Framework

We value SanDisk on a forward P/E basis applied to FY27 full year earnings, the most appropriate time horizon given the earnings inflection currently underway.

FY27 Full Year EPS: $332

The multiple question is the most important analytical decision in this valuation. The market has historically applied 5x to 8x earnings to memory companies, reflecting the cyclical discount that volatile, spot-market-driven earnings deserved.

SanDisk is no longer that business. The five LTA contracts with $42 billion in minimum revenue backlog and $11 billion in enforceable financial guarantees represent a structural shift in earnings visibility that the historical commodity multiple does not reflect.

We apply 12x FY27 EPS as our base case multiple. This sits between the commodity discount at 5x to 8x and the full infrastructure re-rating at 20x to 24x that Equinix and Digital Realty command. It reflects a business that has demonstrably reduced its cyclicality through contracted revenue, but has not yet accumulated the multi-year track record that would justify a full infrastructure franchise multiple.

12x is still a significant discount to every comparable contracted infrastructure business. It is the number that requires only one thing - that the NAND shortage persists into 2027 and the five LTA agreements hold. Both conditions are documented, contracted, and legally enforceable.

Bridge To Price Target

FY27 Full Year EPS : $332

Multiple applied : 12x

Implied Price Target : $3,983

Current price : $1,559

Implied Upside : +155%

The Sensitivity Table

For readers who want to stress-test the assumptions:

Bear case - FY 27 EPS : $250, multiple : 10x - Price target $2,500

Base Case - FY 27 EPS : $332, multiple : 12x - Price target $3,983

Bull Case - FY 27 EPS : $400, multiple : 14x - Price target $5,600

Even in the bear case, where our FY27 EPS projection misses by 25%, the implied price of $2,500 represents 60% upside from current levels.

One Honest Caveat

The FY27 model assumes the NAND shortage persists and ASPs continue rising through early 2027. That is the central assumption - and the central risk. If Samsung or Kioxia bring supply online faster than expected, the earnings trajectory compresses. A 12x multiple on lower earnings produces a significantly lower price target.

This is a high-conviction, high-risk position at current prices. The upside is real and large. So is the downside if the cycle turns earlier than modeled. Size accordingly.

Risks

1. Supply Normalisation - The Central Risk

The entire FY27 earnings model rests on one assumption - that the NAND shortage persists through 2026 and into early 2027. If Samsung, Kioxia, or Micron bring meaningful new supply online faster than expected, ASPs normalize and the earnings trajectory compresses rapidly.

This is not a hypothetical risk. Every NAND shortage in history has eventually ended. The question is timing - and timing is the one variable no model can predict with precision. At $1,559 per share and 54x trailing earnings, the stock has limited tolerance for an early cycle turn.

2. Customer Concentration

SanDisk faces high customer concentration risk - a small number of hyperscaler relationships represent the majority of enterprise revenue. The five LTAs (long Term Agreements) provide financial protection against cancellation but do not eliminate the operational dependency on a handful of large customers. A change in procurement strategy at any one of them - a shift to alternative storage architectures, a slowdown in AI infrastructure spending, or a decision to diversify suppliers - would have a disproportionate impact on revenue.

3. Kioxia Dependency and Geopolitical Exposure

SanDisk and Kioxia currently operate three business ventures across eight flash-based manufacturing facilities in Japan. Every wafer SanDisk sells begins its life in a Japanese fabrication plant. Any escalation in regional tensions could disrupt its global supply chain. This is not a Japan-specific risk - it is the concentration of critical semiconductor manufacturing in a geographically constrained region at a time of elevated geopolitical uncertainty. Taiwan Strait tensions, US-China trade policy shifts, and export control escalation all create potential disruption pathways for a supply chain that runs entirely through East Asia.

4. Technology Execution - BiCS and QLC Ramp

Skipping generations - like the rush to BiCS10 - carries the risk of manufacturing defects or lower yields, which could erode margins. SanDisk’s competitive position depends on staying at the leading edge of NAND layer count - more layers per wafer means more bits per wafer which means lower cost per gigabyte. Any yield problem during a technology transition compresses supply and margin simultaneously. QLC Stargate, which has not yet shipped revenue-generating units, carries inherent execution risk as it moves from qualification to high-volume production.

5. Chinese Competition

The NAND market has a new entrant that did not exist at meaningful scale in previous cycles - YMTC, the Chinese state-backed flash memory manufacturer. While currently constrained by US export controls on advanced manufacturing equipment, YMTC has demonstrated the ability to produce competitive NAND at meaningful volumes. Any relaxation of export controls, or any acceleration in China’s domestic semiconductor equipment capabilities, would introduce a new source of supply into an already tightly balanced market.

Our View

Eli Harari walked out of Hughes Aircraft in the 1970s with a theory that semiconductor storage would eventually replace every mechanical storage technology on earth. He was right. It took fifty years - but he was right.

SanDisk was built on that conviction. It survived the acquisition by Western Digital, nine years of invisibility inside a conglomerate, and a February 2025 spinoff at $38.50 that most investors ignored. Then AI arrived. The inference workloads that nobody modelled in the consumer-centric NAND forecasts turned out to require more storage than everything that came before them combined.

The numbers that followed are among the most extraordinary in semiconductor history. Revenue up 251% in five quarters. Gross margins from 23.7% to 78.4%. EPS from -$0.30 to $23.41. A market cap that went from essentially nothing to $230 billion. And a contracted revenue backlog of $42 billion - with $11 billion in enforceable financial guarantees - that has never existed in the NAND industry before.

The easy money has been made. Anyone who bought at the spinoff has already made 4,000%. The question we are asking is a different one - is there still a compelling risk-reward at $1,559?

Our answer is yes. But it requires intellectual honesty about what you are buying.

You are buying the FY27 earnings trajectory - $332 in full year EPS if the shortage persists and the ASP assumptions hold. At 12x that is $3,983. That is 161% upside from today. It is also entirely contingent on a NAND cycle that does not turn early, a Kioxia joint venture that executes without disruption, and a QLC Stargate ramp that delivers what the roadmap promises.

The LTA contracts reduce the downside. They do not eliminate it. A one-third contracted revenue base means two thirds is still exposed to spot market dynamics. The financial penalties protect against cancellation - they do not protect against a world where spot NAND prices fall 40% and the uncontracted portion of the business reprices with them.

This is a high-conviction, high-risk position. The upside is real, large, and defensible. The downside requires only that the cycle turns earlier than management, TrendForce, and our model suggest.

Size accordingly. Hold with conviction. Exit if the supply picture changes materially.

We are long SNDK 0.00%↑